kottke.org posts about economics

Making a sandwich completely from scratch took this guy six months and cost $1500. He grew his own vegetables, made his own butter & cheese, made sea salt from salt water, and harvested wheat for bread flour. And that’s with a few shortcuts…he didn’t raise the cow & chicken from a calf & chick or the bees from a starter hive.

See also I, Pencil, how a can of Coca-Cola is made, and How to Cook Soup.

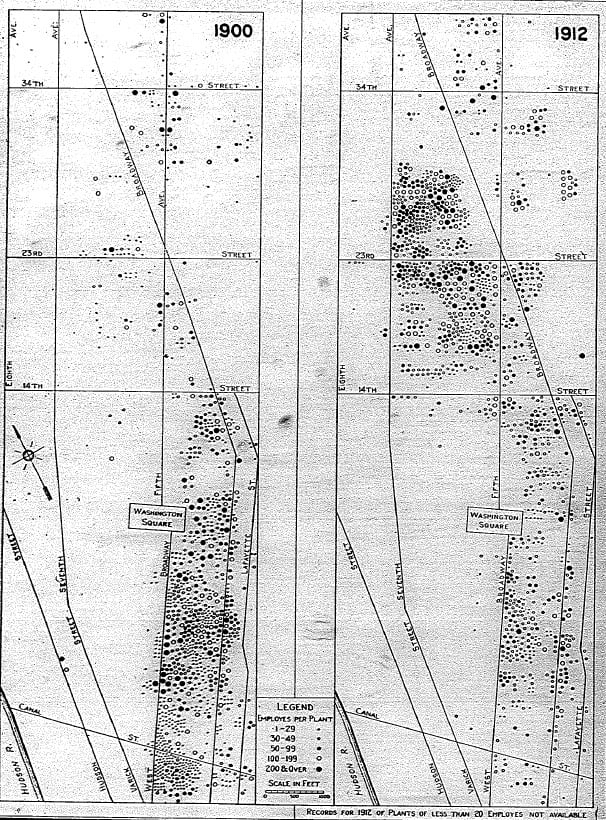

Economist William Easterly and some of his colleagues built a site that focuses on the economic development of a single block in NYC, Greene Street between Houston and Prince. In the past 175 years, use of the block has gone from wealthy residential to sex work to garment manufacturing to artist galleries to luxury retail.

133 Greene Street, for example, has been part of the large Bayard farm, a grand residential home, a brothel, a garment factory, part of a slum, an art gallery, and is today the home of luxury co-op residences and a Dior Homme store.

Many of these shifts took only a decade and could have been very difficult to anticipate.

The site was built to accompany an academic paper on economic development.

By 1870, the Greene Street Block contained 14 brothels, the highest concentration of any block in the City. Just as surprising was the sudden end of prostitution on the block. Brothels still abounded in 1880, but during the next decade entrepreneurs demolished and rebuilt almost the entire block as castiron factories and warehouses, and what was left of the red-light district moved up town.

The site is a little confusing to navigate, but is worth checking out in detail. For instance, check out how quickly the garment manufacturing industry shifted from downtown to the present-day Garment District.

(via wired)

From the abstract of a paper on the relationship between impatience and procrastination, this caught my eye:

We find substantial evidence of time inconsistency. Namely, more that half of the participants who receive their check straight away instead of waiting two weeks for a reasonably larger amount, subsequently take more than two weeks to cash it.

This reminded me of a passage I read recently in Oliver Burkeman’s The Antidote1 about the pitfalls of positive visualization.

Yet there are problems with this outlook, aside from just feeling disappointed when things don’t turn out well. These are particularly acute in the case of positive visualisation. Over the last few years, the German-born psychologist Gabriele Oettingen and her colleagues have constructed a series of experiments designed to unearth the truth about ‘positive fantasies about the future’. The results are striking: spending time and energy thinking about how well things could go, it has emerged, actually reduces most people’s motivation to achieve them. Experimental subjects who were encouraged to think about how they were going to have a particularly high-achieving week at work, for example, ended up achieving less than those who were invited to reflect on the coming week, but given no further guidelines on how to do so.

In one ingenious experiment, Oettingen had some of the participants rendered mildly dehydrated. They were then taken through an exercise that involved visualising drinking a refreshing, icy glass of water, while others took part in a different exercise. The dehydrated water-visualisers — contrary to the self-help doctrine of motivation through visualisation — experienced a significant reduction in their energy levels, as measured by blood pressure. Far from becoming more motivated to hydrate themselves, their bodies relaxed, as if their thirst were already quenched. In experiment after experiment, people responded to positive visualisation by relaxing. They seemed, subconsciously, to have confused visualising success with having already achieved it.

In a similar way, it may be that the people who received their checks right away but didn’t cash them “relaxed” as though they had actually spent the money, not just gotten the check. (via mr)

The Waffle House Index is an informal metric used by FEMA administrator Craig Fugate to evaluate how bad a storm is. Basically, whether the Waffle House in town is open or serving a limited menu can tell you something about how bad the storm was and how much recovery assistance is necessary.

If you get there and the Waffle House is closed? That’s really bad. That’s where you go to work.

See also The Economist’s Big Mac Index and other odd economic indicators. (via @naveen)

Socrates once wrote, “He is richest who is content with the least.” Even the great Greek philosopher would be feeling a little too rich today in Greece where citizens, greeted by news that the nation’s banks would be closed for the week, lined up at ATMs and employed the Socratic method with the repetition of the question: “Where the hell’s my money?” And if you’ve taken a look at your stock portfolio, there’s a decent chance you’ve asked your broker the same question. Here’s an overview of the Greek economic crisis from NYT Upshot, and the latest updates from BBC.

This global economy stuff is all Greek to me. If you’re feeling the same, you might appreciate Quartz’s guide to everything you need to know about this unfolding Greek tragedy, Mashable’s list of the five things you need to know about the meltdown, and Felix Salmon’s helpful explainer.

Michael Lewis explains the Greek financial crisis by comparing it to a Berkeley pedestrian.

He simply wants to stress to you, and perhaps even himself, that he occupies the high ground. In doing so, he happens to increase the likelihood that he will wind up in the back of an ambulance.

About the time Katrina struck, New Orleans was the jail capital of America, incarcerating people at four times the national average. Since that time, the city has reduced its local inmate population by 67%. What was the trick? First, they stopped treating jailing like a business. And second, they built a smaller jail. No really. That was a key factor. And get this; during the period New Orleans stopped jailing so many people, there has been an overall reduction in crime. Smaller jails. Less crime. Jazz hands.

[This item is syndicated from Nextdraft, but I had to add a little something about induced demand. Like building bigger roads resulting in more traffic (not less), building bigger jails means you want to fill them with criminals. Kudos to New Orleans for building a smaller jail and finding ways to adjust to the reduced supply of jail cells. -jkottke]

The Atlantic’s Derek Thompson examines the act of giving and goes in search of the best charitable cause in the world.

Perhaps the most piercing lesson from effective altruism is that one can make an astonishing difference in the world with a pinch of logic and dash of math.

See also Doing Good Better.

Tyler Cowen was recently asked how he’d best use a time machine for financial gain. Here was the specific query:

Suppose you had a time machine you that you solely wanted to use for financial gain. You can bring one item from the present back to any point in the past to exchange for another item that people of that time would consider of equal value, then bring that new item back to the present. To what time period would you go, and what items would you choose to maximize your time-travel arbitrage?

Cowen notes some difficulty with an obvious approach:

The obvious answer encounters some difficulties upon reflection. Let’s say I brought gold back in time and walked into the studio of Velazquez, or some other famous painter, and tried to buy a picture for later resale in the present. At least some painters would recognize and accept the gold, and gold is highly valuable and easy enough to carry around. Some painters might want the gold weighed and assayed, but even there the deal would go fine.

The problem is establishing clear title to the painting, once you got back home. It wouldn’t turn up on any register as stolen, but still you would spend a lot of time talking to the FBI and Interpol. The IRS would want to know whether this was a long-term or short-term capital gain, and you couldn’t just cite Einstein back to them. They also would think you must have had a lot of unreported back income.

So establishing present ownership of a past item is an issue…as is authentication via carbon dating. I don’t have a specific scheme in mind, but I would think any general approach would also need to minimize the butterfly effect of your trade so that, for example, your existence in the present is not disrupted. So you can’t trade Leonardo an iPhone 6 for the Mona Lisa. But maybe you could trade $1 for a winning ticket for last week’s $300 million lottery jackpot…or would the numbers change somehow because of your visit? What if you bought 100,000 shares of Apple stock in 2003? How would that action effect the present? What is a large enough action to make you rich but with a small enough effect to keep the present otherwise unchanged? Since I didn’t see any super-compelling solutions in the comments at MR, I’m gonna open the comments here…I know someone has been thinking about this extensively or has a link to a good discussion elsewhere. Please stay on topic, mmm’kay?

I saw Mad Max: Fury Road yesterday (enjoyed it) but have a few questions.

1. With gasoline in such short supply, I’m surprised the various groups in the movie didn’t take more advantage of solar power to generate energy for electric vehicles and such. Sunshine is obviously abundant in post-apocalyptic Australia and from the looks of what was scavenged from before the nuclear war and the ingenuity on display in getting what they found to function, they should have been able to find even rudimentary solar cells and get them to work.

2. Speaking of energy scarcity, I wonder if the troop-pumping-up and opponent-intimidating function of the flamethrowing guitar player was worth all of the fuel spewed out of the end of his instrument and energy consumed by the incredible number of speakers on his rig.

3. The roads in the movie were in remarkable shape, aside from the swampland. Who was responsible for their upkeep? Even dirt roads need maintenance or they develop potholes and washboarding. And for what reason were they kept in such good condition outside of the Citadel/Gas Town/Bullet Farm area? Aside from Furiosa’s Rig, the chase party, and two smallish motorcycle gangs, I saw no other vehicular traffic on the roads…and who would have been semi-regularly traveling out past the canyon anyway? To where? For what?

4. What was the political and economic arrangement between the Citadel, Gas Town, and the Bullet Farm? Did the Citadel trade their water and crops for gas and bullets? Or was Immortan Joe, as the defender of the lone source of abundant fresh water in the region, the defacto leader of all three groups? The People Eater and Bullet Farmer certainly came a’running when Joe needed help retrieving his wives. There were obviously other sources of water in the region — how else did the biker gangs survive? — so you’d think that Gas Town and the Bullet Farm could have teamed up to squeeze Joe into giving them a better deal or even overthrowing him. Point is, there seemed to be a surprising lack of political friction between the three groups, which seems odd in an environment of scarcity.

5. Surely land was plentiful enough that large solar stills could have generated enough fresh water for people to live on without having to rely on the Citadel for it.

Update: Reddit has a go at answering some of these questions. (via @pavel_lishin)

Shuttered storefronts. Abandoned retail locations. Small businesses that fall like the House of Cards & Curiosities on Eighth Avenue. These are the signs of urban blight we usually associate with economic downturns or poor, forgotten neighborhoods. But these shuttered storefronts are in one of America’s wealthiest neighborhoods; NYC’s West Village. As The New Yorker’s Tim Wu explains, some urban blight emerges when economic times are too good and rents get too high. And we’re not just talking about mom and pop here. Even Starbucks is closing some Manhattan locations due to rent hikes.

Wine ratings are all over the place, particularly when price enters the picture. This video explains that the most expensive wine is not always the best tasting wine, but you might prefer it anyway.

(via @riondotnu)

If you’ve bought a ticket to an event in the past, oh, 15-20 years, chances are you got it from Ticketmaster. Chances are also pretty good that you think Ticketmaster completely sucks, mostly because of the unavoidable and exorbitant convenience fee they charge. And that probably has you wondering: if everyone who uses the service hates Ticketmaster so much, how are they still in business? Because ticket buyers are not Ticketmaster’s customers. Artists and venues are Ticketmaster’s real customers and they provide plenty of value to them.

Ticketmaster sells more tickets than anybody else and they’re the biggest company in the ticket selling game. That gives them certain financial resources that smaller companies don’t have. TM has used this to their advantage by moving the industry toward very aggressive ticketing deals between ticketing companies and their venue clients. This comes in the form of giving more of the service charge per ticket back to the venue (rebates), and in cash to the venue in the form of a signing bonus or advance against future rebates. Venues are businesses too and, thus, they like “free” money in general (signing bonuses), as well as money now (advances) versus the same money later (rebates).

Read that whole Quora answer again…there’s nothing in there about TM being helpful for ticket buyers. It turns out asking “who’s the customer?” is a great way of thinking about when certain companies or industries do things that aren’t aligned with good customer service or user experience.1

Take Apple and Google for instance. Apple sells software and hardware directly to people; that’s where the majority of their revenue comes from. Apple’s customers are the people who use Apple products. Google gets most of their revenue from putting advertising into the products & services they provide. The people who use Google’s products and services are not Google’s customers, the advertisers are Google’s customers. Google does a better job than Ticketmaster at providing a good user experience, but the dissonance that results between who’s paying and who’s using gets the company in trouble sometimes. See also Facebook and Twitter, among many others.

Newspapers, magazines, and television networks have dealt with this same issue for decades now.2 They derive large portions of their revenue from advertisers and, in the case of the TV networks, from the cable companies who pay to carry their channels. That results in all sorts of user hostile behavior, from hiding a magazine’s table of contents in 20 pages of ads to shrieking online advertising to commercials that are louder than the shows to clunky product placement to trimming scenes from syndicated shows to cram in more commercials. From ABC to Vogue to the New York Times, you’re not the customer and it shows.

This might be off-topic (or else the best example of all), but “who’s the customer?” got me thinking about who the customers of large public corporations really are: shareholders and potential shareholders. The accepted wisdom of maximizing shareholder value has become an almost moral imperative for large corporations. The needs of their customers, employees, the environment, and the communities in which they’re located often take a backseat to keeping happy the big investment banks, mutual funds, and hedge funds who buy their stock. When providing good customer service and experience is viewed by companies as opposite to maximizing shareholder value, that’s a big problem for consumers.

Update: I somehow neglected to include the pithy business saying “if you’re not paying for the product, you are the product”, which originated in a slightly different phrasing on MetaFilter.

Update: One example of how maximizing shareholder value can work against good customer service comes from a paper by a trio of economists. In it, they argue that co-ownership of two or more airlines by the same investor results in higher prices.

In a new paper, Azar and co-authors Martin C. Schmalz and Isabel Tecu have uncovered a smoking gun. To test the hypothesis that institutional investors gain market power that results in higher prices, they examine airline routes. Although we think of airlines as independent companies, they are actually mostly owned by a small group of institutional investors. For example, United’s top five shareholders — all institutional investors — own 49.5 percent of the firm. Most of United’s largest shareholders also are the largest shareholders of Southwest, Delta, and other airlines. The authors show that airline prices are 3 percent to 11 percent higher than they would be if common ownership did not exist. That is money that goes from the pockets of consumers to the pockets of investors.

How exactly might this work? It may be that managers of institutional investors put pressure on the managers of the companies that they own, demanding that they don’t try to undercut the prices of their competitors. If a mutual fund owns shares of United and Delta, and United and Delta are the only competitors on certain routes, then the mutual fund benefits if United and Delta refrain from price competition. The managers of United and Delta have no reason to resist such demands, as they, too, as shareholders of their own companies, benefit from the higher profits from price-squeezed passengers. Indeed, it is possible that managers of corporations don’t need to be told explicitly to overcharge passengers because they already know that it’s in their bosses’ interest, and hence their own. Institutional investors can also get the outcomes they want by structuring the compensation of managers in subtle ways. For example, they can reward managers based on the stock price of their own firms — rather than benchmarking pay against how well they perform compared with industry rivals — which discourages managers from competing with the rivals.

(via @krylon)

Today’s drop in crude-oil prices, which began in the summer of 2014, may be as disruptive as the quadrupling of oil prices that created the oil shock of 1974.

For most of us, lower oil prices simply translate as better prices at the gas pump. But the value of oil has big consequences around the world. From Moisés Naím in The Atlantic: The Hidden Effects of Cheap Oil.

From Charlie Brooker’s Weekly Wipe, here’s how every single news report on the economy plays out:

Dennis and Pamela People are affected by numbers, and since they have a child, you’ll empathize with what they say while I nod in their direction.

“Well, it’s been hard because of the numbers.”

“Yeah, it has been hard, mainly because of the numbers.”

Brooker, you may remember, is the creator of Black Mirror.

From Marginal Revolution University, three short videos on the economic concepts of supply, demand, and equilibrium using oil as an example good.

In their latest full episode, Radiolab examines the concept of worth, particularly when dealing with things that are more or less priceless (like human life and nature).

This episode, we make three earnest, possibly foolhardy, attempts to put a price on the priceless. We figure out the dollar value for an accidental death, another day of life, and the work of bats and bees as we try to keep our careful calculations from falling apart in the face of the realities of life, and love, and loss.

I have always really liked Radiolab, but it seems like the show has shifted into a different gear with this episode. The subject seemed a bit meatier than their usual stuff, the reporting was close to the story, and the presentation was more straightforward, with fewer of the audio experiments that some found grating. I spent some time driving last weekend and I listened to this episode of Radiolab, an episode of 99% Invisible, and an episode of This American Life, and it occurred to me that as 99% Invisible has been pushing quite effectively into Radiolab’s territory, Radiolab is having to up their game in response, more toward the This American Life end of the spectrum. Well, whatever it is, it’s great seeing these three radio shows (and dozens of others) push each other to excellence.

The food is fresh. Natural. Locally sourced. Sometimes even organic. That might sound like your local farmer’s market, but it’s actually part of a new and growing movement in the fast-food industry. Think Shake Shack, Chipotle, Panera. While we’re not exactly seeing tractors in the drive-thrus, the rise of these chains (and the pressure on their predecessors that placed a lot more emphasis on the fast than the food) tell us a lot about economic inequality, the modern workday, and fries. From The New Yorker’s James Surowiecki: The Shake Shack Economy.

Steven Brill has written a book about the making of the Affordable Care Act called America’s Bitter Pill: Money, Politics, Backroom Deals, and the Fight to Fix Our Broken Healthcare System.

America’s Bitter Pill is Steven Brill’s much-anticipated, sweeping narrative of how the Affordable Care Act, or Obamacare, was written, how it is being implemented, and, most important, how it is changing — and failing to change — the rampant abuses in the healthcare industry. Brill probed the depths of our nation’s healthcare crisis in his trailblazing Time magazine Special Report, which won the 2014 National Magazine Award for Public Interest. Now he broadens his lens and delves deeper, pulling no punches and taking no prisoners.

Malcolm Gladwell has a review in the New Yorker this week.

Brill’s intention is to point out how and why Obamacare fell short of true reform. It did heroic work in broadening coverage and redistributing wealth from the haves to the have-nots. But, Brill says, it didn’t really restrain costs. It left incentives fundamentally misaligned. We needed major surgery. What we got was a Band-Aid.

I haven’t read his book yet, but I agree with Brill on one thing: the ACA1 did not go nearly far enough. Healthcare and health insurance are still a huge pain in the ass and still too expensive. My issues with healthcare particular to my situation are:

- As someone who is self-employed, insurance for me and my family is absurdly expensive. After the ACA was enacted, my insurance cost went up and the level of coverage went down. I’ve thought seriously about quitting my site and getting an actual job just to get good and affordable healthcare coverage.

- Doctors aren’t required to take any particular health insurance. So when I switched plans, as I had to when the ACA was enacted, finding insurance that fit our family’s particular set of doctors (regular docs, pediatrician, pediatric specialist that one of the kids has been seeing for a couple of years, OB/GYN, etc.) was almost impossible. We basically had one plan choice (not even through the ACA marketplace…see next item) or we had to start from scratch with new doctors.

- Many doctors don’t take the ACA plans. My doctor doesn’t take any of them and my kids’ doc only took a couple. And they’re explicit in accepting, say, United Healthcare’s regular plan but not their ACA plan, which underneath the hood is the exact same plan that costs the same and has the same benefits. It’s madness.

- The entire process is designed to be confusing so that insurance companies (and hospitals probably too) can make more money. I am an educated adult whose job is to read things so they make enough sense to tell others about them. That’s what I spend 8+ hours a day doing. And it took me weeks to get up to speed on all the options and pitfalls and gotchas of health insurance…and I still don’t know a whole lot about it. It is the most un-user-friendly thing I have ever encountered.

The ACA did do some great things, like making everyone eligible for health insurance and getting rid of the preexisting conditions bullshit, and that is fantastic…the “heroic work” mentioned by Gladwell. But the American healthcare system is still an absolute shambling embarrassment when you compare it to other countries around the world, even those in so-called “developing” or “third world” countries. And our political system is just not up to developing a proper plan, so I guess we’ll all just limp along as we have been. Guh.

Legal scholar Cass Sunstein presents his annual list of the movies that best showcased behavioral economics for 2014.

Best actor: In 1986, behavioral scientists Daniel Kahneman and Dale Miller developed “norm theory,” which suggests that humans engage in a lot of counterfactual thinking: We evaluate our experiences by asking about what might have happened instead. If you miss a train by two minutes, you’re likely to be more upset than if you miss it by an hour, and if you finish second in some competition, you might well be less happy than if you had come in third.

“Edge of Tomorrow” spends every one of its 113 minutes on norm theory. It’s all about counterfactuals — how small differences in people’s actions produce big changes, at least for those privileged to relive life again (and again, and again). Tom Cruise doesn’t get many awards these days, or a lot of respect, and we’re a bit terrified to say this — but imagine how terrible we’d feel if we didn’t: The Top Gun wins the Becon.

(via @tylercowen)

Scenes from Seinfeld can help illustrate economic concepts like incentives, thinking at the margin, and common resources. For instance, in The Strike from season nine (the episode that popularized Festivus), Elaine angles for a free sandwich:

Elaine has eaten 23 bad sub sandwiches, and if she eats a 24th, she’ll get one free. She is determined to do it, even though Jerry advises her to ignore sunk costs and walk away.

See also the economics of The Simpsons.

Michael Lewis on a new book about billionaires, the increasing economic inequality in America, and the impact of the behavior of the very rich is having on politics and happiness. The camp breakfast anecdote at the beginning of the article is gold.

You all live in important places surrounded by important people. When I’m in the big city, I never understand the faces of the people, especially the people who want to be successful. They look so worried! So unsatisfied!

In the city you see people grasping, grasping, grasping. Taking, taking, taking. And it must be so hard! To be always grasping-grasping, and taking-taking. But no matter how much they have, they never have enough. They’re still worried. About what they don’t have. They’re always empty.

You have a choice. You don’t realize it, but you have a choice. You can be a giver or you can be a taker. You can get filled up or empty. You make that choice every day. You make that choice at breakfast when you rush to grab the cereal you want so others can’t have what they want.

The piece is filled with Lewis-esque observations throughout. Like:

Rich people, in my experience, don’t want to change the world. The world as it is suits them nicely.

And:

The American upper middle class has spent a fortune teaching its children to play soccer: how many great soccer players come from the upper middle class?

But the studies about the effects of wealth and privilege on human behavior are what caught my eye the most.

In one study, Keltner and his colleague Paul Piff installed note-takers and cameras at city street intersections with four-way stop signs. The people driving expensive cars were four times more likely to cut in front of other drivers than drivers of cheap cars. The researchers then followed the drivers to the city’s cross walks and positioned themselves as pedestrians, waiting to cross the street. The drivers in the cheap cars all respected the pedestrians’ right of way. The drivers in the expensive cars ignored the pedestrians 46.2 percent of the time — a finding that was replicated in spirit by another team of researchers in Manhattan, who found drivers of expensive cars were far more likely to double park.

Living in Manhattan, I see stuff like this all the time and it’s becoming increasingly difficult to think of the rich and privileged as anything other than assholes, always grasping, grasping, grasping, taking, taking, taking.

We the Economy is a series of 20 short videos that attempt to explain important economic concepts. For instance, acclaimed director Ramin Bahrani did a video about regulatory capture starring Werner Herzog, Patton Oswalt, and the Sherman Antitrust Act of 1890.

Anchorman director Adam McKay directed an animated My Little Pony-esque video about wealth distribution and income inequality featuring the voice talents of Amy Poehler, Maya Rudolph, and Sarah Silverman.

Paul Allen and Morgan Spurlock are behind the effort, with Bob Balaban, Steve James, Catherine Hardwicke, and Mary Harron directing some of the other videos. (via mr)

Mark Bittman on the true cost of producing a hamburger, after accounting for externalities like carbon generation and obesity.

Cheeseburgers are the coal of the food world, with externalities in spades; in fact it’s unlikely that producers of cheeseburgers bear the full cost of any aspect of making them.

This made me think of something I wrote for Worldchanging several years ago about a True Cost rating:

Wealth doesn’t just magically materialize into your bank account. It comes from the ground, human effort, the flesh of animals, the sun, and the atom. The global economy is driven by nature, and yet it’s not usually found on the accountant’s balance sheet. Perhaps it should be. I’d like to know the true cost of the stuff I buy. Embodied energy and carbon footprint calculations are a good start, but it would be nice if the product itself came with a True Cost number or rating, like the nutritional information on a cereal box or the Energy Star rating on a refrigerator.

When True Cost is factored in, conflict diamonds become a morally expensive choice to make when they’re fueling turmoil in the world. Likewise clothing made in sweatshops. Organic tomatoes flown in from Chile may be less expensive at the register, but how much carbon dioxide was released into the atmosphere flying/driving them to your table? What’s the energy cost of living in the suburbs compared to living downtown? Do the people who made the clock hanging on my wall get paid a fair wage and receive healthcare? Just how bad for the environment is the laptop on which I’m typing?

(via subtraction)

Two dozen people offer you their best advice on how to invest a single dollar.

I don’t have any awesome ideas for how to invest a buck, unfortunately. That is my weakness. My first instinct was to invest it in a stripper’s g-string or a barista’s tip jar. But I’m not sure how that translates as investment. I do know that the more frequently you visit/tip a barista — your neighborhood barista, who does not work at a Starbucks — the more often you are treated like family and you get free coffee. I think that the more you invest in a stripper, the less you get free things from that stripper.

Over the course of his 3000 columns at The Motley Fool, Morgan Housel has learned a few things:

I’ve learned that short-term thinking is at the root of most of our problems, whether it’s in business, politics, investing, or work.

I’ve learned that debt can cause more social problems than some drugs, yet drugs are illegal and debt is tax deductible.

I’ve learned that finance is actually very simple, but it’s made to look complicated to justify fees.

Unfortunately, the list is undermined almost completely by the get-rich-quick advertising on the site, including this bit at the end of the article, which I can’t even tell is an ad or just a promotion:

Opportunities to get wealthy from a single investment don’t come around often, but they do exist, and our chief technology officer believes he’s found one. In this free report, Jeremy Phillips shares the single company that he believes could transform not only your portfolio, but your entire life. To learn the identity of this stock for free and see why Jeremy is putting more than $100,000 of his own money into it, all you have to do is click here now.

Short-term thinking is at the root of most of our problems, click here now. Now!

A group led by Dr. Robert Costanza has calculated the value of the world’s ecosystems…the group’s most recent estimate puts the yearly value at $142.7 trillion.

“I think this is a very important piece of science,” said Douglas J. McCauley of the University of California, Santa Barbara. That’s particularly high praise coming from Dr. McCauley, who has been a scathing critic of Dr. Costanza’s attempt to put price tags on ecosystem services.

“This paper reads to me like an annual financial report for Planet Earth,” Dr. McCauley said. “We learn whether the dollar value of Earth’s major assets have gone up or down.”

The group last calculated this value back in 1997 and it rose sharply over the past 17 years, even as those natural habitats are disappearing. This line from the article stunned me:

Dr. Costanza and his colleagues estimate that the world’s reefs shrank from 240,000 square miles in 1997 to 108,000 in 2011.

Coral reefs shrank by more than half over the past 17 years…I had no idea the reef situation was that bad. Jesus.

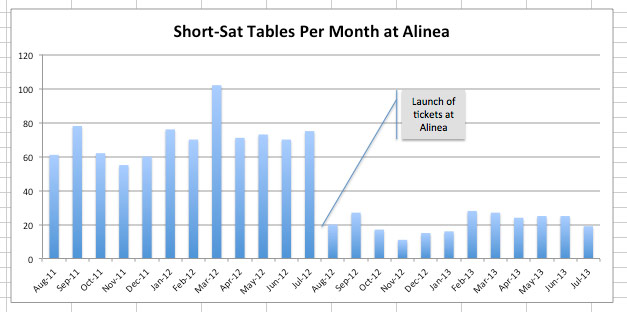

For three years, Nick Kokonas’s trio of eating/drinking establishments in Chicago (Next, Alinea, and Aviary) has been using a ticketed reservation system. In this epic piece, Kokonas details why they started using tickets and what the effect has been (emphasis mine):

Our ticket implementation strategy at Alinea was to create a “higher-touch” system than we had previously used at Next. Every customer buying a ticket at Alinea must include a cell phone number where we can reach them. About a week before they dine with us we call every customer to thank them for buying a ticket to Alinea, ask if they have any dietary restrictions or special needs, and generally get a feel for their expectations and whether it is a special occasion. We can, in fact, spend more time (not less) with every single one of our customers because we are only speaking with the customers we know are coming to dine with us. Previously, we answered thousands of calls from people we had to say ‘no’ to. Now we can take far more time to say ‘yes’.

The results on Alinea’s business are staggering. Bottom line EBITDA profits are up 38% from previous average years. No shows of full tables are almost non-existent and while partial no-shows still occur they are only a handful of people per week at most. That allows us to run at a far greater capacity with less food waste and more revenue.

Will be interesting to see if more restaurants adopt this model…I bet a bunch of restaurateurs’ eyes lit up at the 38% increase in profit. But not every restaurant is Alinea and not every restaurateur is a clever former derivatives trader.

Mike Merrill reimagines the game of Monopoly to better represent the modern financial system by adding the banker as a player, convertible notes, and Series A financing.

Each player starts with only $500. That’s a nice bit of cash, but it’s going to be expensive to build your capitalist empire. Baltic Avenue will cost you $80, States Avenue is $140, Atlantic is $260, and that leaves you just $20. Even if you’re the first to land on Boardwalk you won’t be able to afford the $400 price tag. Another $200 from “passing Go” is not going to last that long. You need more money.

At the start of the game the banker will offer each player a convertible note of $1000 at a 20% discount and 5% interest*. Armed with $1500 the player is now ready to set out on their titan of the universe adventure! (Of course players are not required to take the convertible note.)

That sounds fun? (via waxy)

Steven Levitt and Stephen Dubner, the co-authors of the immensely popular Freakonomics, are back with their third book in the series: Think Like a Freak. In it, rather than discussing what they think, they talk about how they think.

Levitt and Dubner offer a blueprint for an entirely new way to solve problems, whether your interest lies in minor lifehacks or major global reforms. As always, no topic is off-limits. They range from business to philanthropy to sports to politics, all with the goal of retraining your brain. Along the way, you’ll learn the secrets of a Japanese hot-dog-eating champion, the reason an Australian doctor swallowed a batch of dangerous bacteria, and why Nigerian e-mail scammers make a point of saying they’re from Nigeria.

The book is out on May 12, but of course you can preorder, etc.

Update: Excerpt in the WSJ.

Homer Economicus is a new book which uses the fictional world of Springfield on The Simpsons to explain the basic concepts of economics.

Since The Simpsons centers on the daily lives of the Simpson family and its colorful neighbors, three opening chapters focus on individual behavior and decision-making, introducing readers to the economic way of thinking about the world. Part II guides readers through six chapters on money, markets, and government. A third and final section discusses timely topics in applied microeconomics, including immigration, gambling, and health care as seen in The Simpsons. Reinforcing the nuts and bolts laid out in any principles text in an entertaining and culturally relevant way, this book is an excellent teaching resource that will also be at home on the bookshelf of an avid reader of pop economics.

(via mr)

Newer posts

Older posts

Socials & More